Cash Don’t Lie #1: Bulls*it Earnings

Cash Don’t Lie is a series of blog posts on entrepreneurial finance

Charlie Munger once famously quipped at a Berkshire Hathaway shareholder meeting, “I think that every time you see the word EBITDA, you should substitute the word ‘bullsh*t’ earnings.”

Part of every finance lead’s job, no matter the size or scale of the firm, is to weave the numbers with an (accurate) storytelling. For some managers, there is an element of surprise each month, when there is friction between EBITDA and the underlying economic reality.

As a reminder, EBITDA stands for Earnings Before Interest Taxes Depreciation and Amortization. Over the years, it has become a preferred metric by investors and operators alike in underwriting as a proxy for a company’s cash flowing ability. If used in isolation, however, some EBITDA pitfalls are as follows:

CapEx Intensity: For CapEx intensive companies (such as acquisition companies) whose business model requires heavy investment into fixed assets and long term capitalized assets, EBITDA provides potentially misleading guidance in assessing the cash flow ability of the enterprise. Capital expenditures, investments, and large prepaid expenses only hit the P&L in the form of depreciation, amortization, or impairment - all of which can be thought of as “below the line” EBITDA items. In short, there will always be a lag between these types of cash outflows and the expense line item on the P&L associated with it, which can take several years to fully exhaust.

One-time expenses: Because EBITDA is intended to represent steady-state operating performance, “one-time” expenses are generally excluded. You’ll often see consulting engagements, certain R&D projects, litigation expenses, and moving expenses can fall into this category. While EBITDA does not include items that are nonrecurring in nature, these items in aggregate can have a tendency to find their way onto the lower part of the income statement frequently enough that it makes them appear not so one-time nature-y.

GAAP Accounting: EBITDA is a non-GAAP metric, which means that it is not officially delineated on a P&L, although it is still comprised of GAAP accounting numbers, which has its own set of idiosyncrasies, some of which are below:

A revenue recognition entry alone won’t tell you anything about turnover, or the ability of the company to collect.

Large cash inflows won’t get credit (pun sort of intended I guess) on the P&L if those revenues are unearned, and they instead, sit on the balance sheet as a liability until the obligation is satisfied. Percentage of completion accounting is another area we won’t bore you with where cash flow will need to be reconciled due to timing differences. Unrealized gains, by definition, won’t translate into cash in right away and are sometimes included in EBITDA.

As Michael Mauboussin and others have pointed out, how we think about “investments” is based on somewhat archaic rules that are not really reflective of modern times. As sort of the inverse of issue #1 on CapEx intensity, take a SaaS company or services company for example. We view these types of businesses as a "capital-light” because of very low, if any, CapEx requirements and because they don't have a ton of tangible assets on their book. This does not mean, however, that these businesses aren’t "investing" in growth. The investments of these types of companies are instead recorded on the P&L, expensed as incurred. When you think about it, should a great social media ad be thought of differently than any other amortizable asset? Investments in growth under GAAP arguably have uneven treatment, and therefore, this could put sandbags on the reported EBITDA number.

We’ve seen that it’s not uncommon for very early-stage companies with less sophisticated accounting practices to apply a hybrid cash/accrual approach by which some revenues are recognized on an accrual basis (as revenues are earned and before cash is collected), while many expenses are recognized on a cash basis (only incurred as paid). This can potentially understate expenses on the P&L and thus, the potential for EBITDA overstatement.

Management discretion: Touching upon all the points made above, whenever management discretion is involved, it means that sometimes, the batter is also the umpire. So the user needs to understand the assumptions if any that underlie the numbers where appropriate. For example, the amortization of their content makes up the majority of Netflix’s cost of revenues. It would behoove a prospective investor to understand how Netflix approaches this expense.

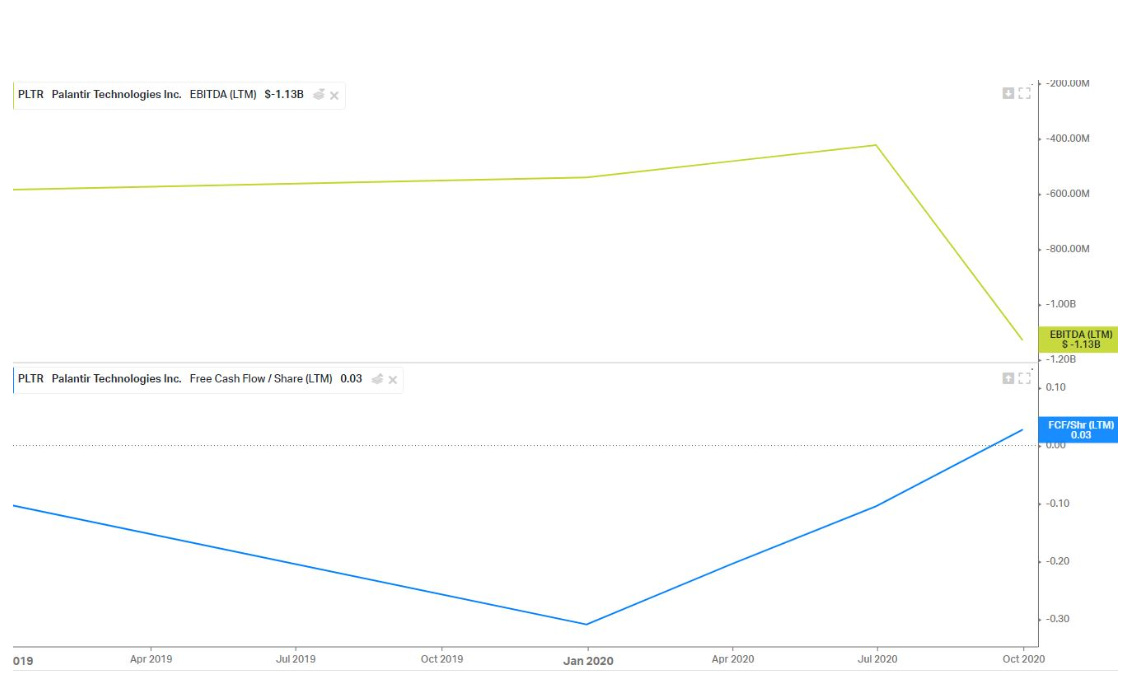

It's therefore not uncommon to see FCF and EBITDA discrepancies, such as Palantir's LTM figures (see graph below):

Source: Koyfin

Of course, this is just referring to “old school” EBITDA. These days, “Adjusted EBITDA” and whatever names come along with it, often have so many addbacks and bells and whistles attached, that the metric appears unrecognizable when compared to cash flows.

Which reminds me of this meme:

Therefore, some early-stage and cash-burning companies who internally place an overemphasis on EBITDA as their cash generation metric could end up with a higher burn rate in the intermediate-term while finding themselves staring at a shorter runway than anticipated. It is not uncommon for a management team to ask themselves “I don’t understand how we have X months of runway, when we’ve been EBITDA positive for X amount of months.”

The reality for operators is that EBITDA is still significant as the often preferred metric for outsiders. Private funds and operators look at EBITDA margin expansion as proof of value creation, and of course, there is validity to that.

EBITDA cannot simply be ignored, but rather, it is best used when taken in context with “the story.” We also think it is best suited as an external metric. That is, until someone comes along and does for financial KPIs what Bill James, and later Billy Beane and Paul DePodesta, did for baseball statistics.

To conclude post #1, we wouldn’t quite call EBITDA “bullsh*t earnings” (although I respect the passion) however, if not careful, using it in isolation can be misleading. Maybe instead, we’d call it “Earnings that require further analysis and maybe also look at TTM free cash flows, to see if they somewhat mirror each other, to see if it checks out.”

That doesn’t roll off the tongue quite as well.

In the next post, we will cover how we think operators should think about healthier internal cash flow and liquidity metrics.

—

If you enjoyed this post, we’d love for you to subscribe/share it with others:

—

This is a personal blog collaboration. All views and opinions expressed are those of the authors and do not reflect the views or opinions of any organizations the authors may be affiliated with. This website and the information contained herein is not intended to be a source of advice with respect to the material presented, and the information contained in this website does not constitute investment, tax, or legal advice. We make no representations as to the accuracy, completeness, correctness, suitability, or validity of any information on this site.