Love & Hate: Issue #1 – Good Credit Products and Bad Forecasts

A CrossStack sub-blog on the good, the bad, and the ugly in the world of finance

Love:

When you design a credit product whose repayment risk is not derived from the party seeking credit.

A wise credit guy once said, “you want to lend to those who don’t need money, and not lend to those who do need the money.” It seems counterintuitive, but the point is true: those seeking credit are, by definition, worse credits – because they are in need for liquidity that they don’t otherwise have.

Think of an unsecured loan: a person wants to remodel their kitchen, pay for a vacation they can’t afford, or go back to school – but they lack the funds, so they borrow. Seems innocuous enough, and there’s a trillion-dollar market for these kinds of loans.

A better lending approach is having collateral – like a mortgage, which is secured by one’s home. You have the same borrower as you did previously, with way too little to pay for a home in cash, but a bank lends to them because there is something securing the payback. Default rates for secured loans are lower than for unsecured for that reason. I’m not telling you anything new here.

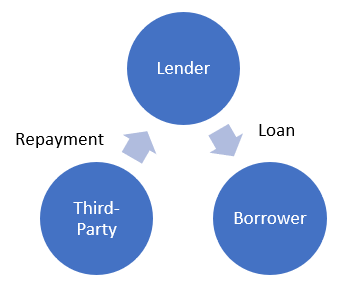

But what if you could lend to a borrower who needs credit, secured by a payback obligation from a third-party who doesn’t? It’s hard to find these credits, but when you do, it’s magical.

Here are a few examples:

Factoring is a good one: you lend to a business, and then you re-direct their accounts receivable so that you capture the money owed to it before it even hits their bank account

Insurance premium finance is another: you lend money to pay insurance premiums for the year, and if the borrower doesn’t pay you back, you cancel their insurance and get a refund for the remaining premiums from the insurance company (genius)

A loan to a landlord secured by the rental payments of the tenant: the landlord is the one in need of capital, but the repayment of the loan is secured by the cashflows of a high-quality tenant

When you see a structure like this – a “credit triangle,” if you will – it’s a special kind of credit that will intrinsically perform better than all others.

Hate:

When you have $0 of revenue today, and you’re showing a pro forma forecast that gets to $1bn of EBITDA in 3 years.

Surprisingly, I actually had founders show me forecasts like these.

It makes us wonder, does the founder appreciate how few companies actually earn $1bn of EBITDA? Let alone how few companies get to that number in just 3 years?

The fact that the founder presents such an optimistic forecast suggests a lack of judgement in a way that diminishes other assumptions made by an operator.

Moreover, putting a forecast like that in front of investors and expecting them to be impressed suggests that either: (i) the founder thinks they will outpace Bill Gates or Steve Jobs, neither of whom had $1bn of EBITDA in 3 years, (ii) there’s too much hubris, or (iii) the founder thinks that over-selling will fool us into giving overly generous terms.

Be realistic! When I see overly optimistic forecasts, I tend to severely discount them. When I see low forecasts, I think the entrepreneur is conservative – which gives them more credibility with respect to everything else.

—

If you enjoyed this post, we’d love for you to share it with others:

—

This is a personal blog collaboration. All views and opinions expressed are those of the authors, and do not reflect the views or opinions of any organizations the authors may be affiliated with. This website and the information contained herein is not intended to be a source of advice with respect to the material presented, and the information contained in this website does not constitute investment, tax, or legal advice. We make no representations as to the accuracy, completeness, correctness, suitability, or validity of any information on this site.