The Amazon Third Party Seller Ecosystem Might be the Most Important Thing Since the iOS App Store

I began following the Amazon Third Party Seller market last year, and have started to believe it’s the most important thing to have happened since the iOS app store.

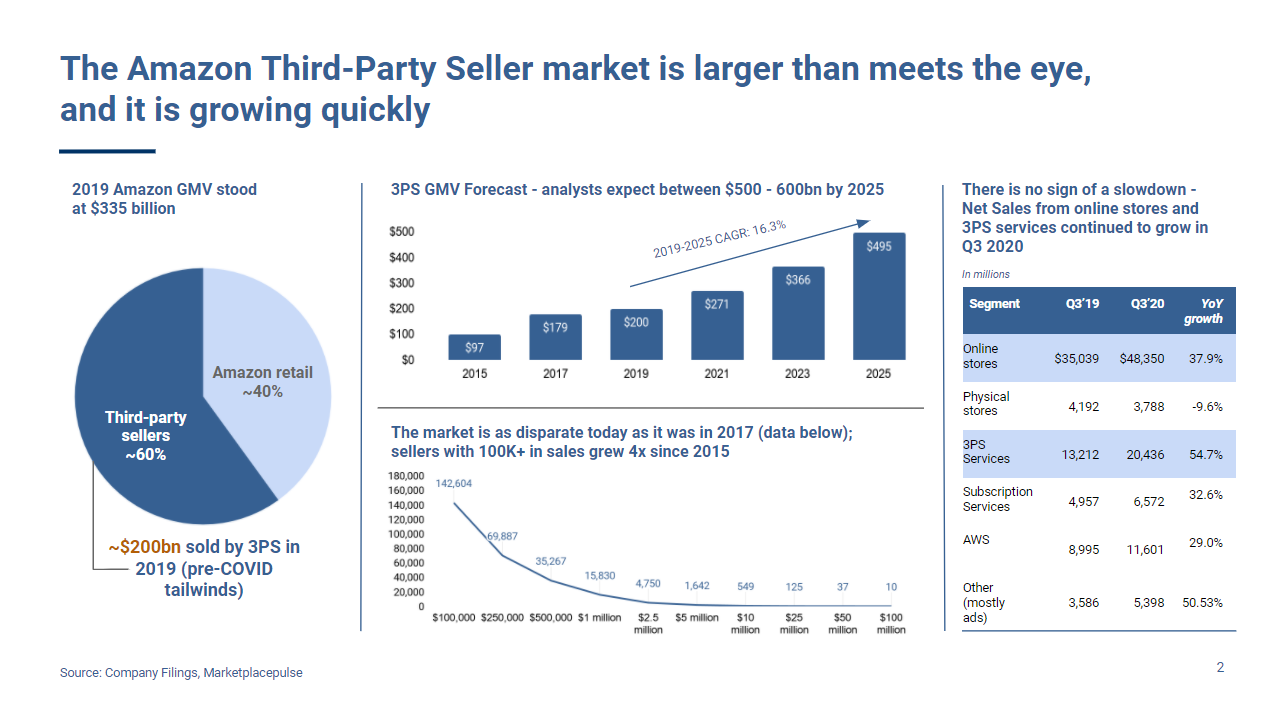

Amazon Third Party sellers use the Fulfilled By Amazon (FBA) program to sell products through the Amazon store. It’s shocking to me – but most people don’t realize how big the market is. When I ask my smartest friends in finance: “have you spent any time thinking about Amazon FBA?” the overwhelmingly common answer is “no.”

But it is expected that ~$200B of sales will go through the marketplace this year, and most analysts expect that number to reach $400B by 2023. It is the first $1T+ asset class that will get developed, almost from scratch, during my career as an investor (I bet it’ll reach $1T even before crypto hits a $1T market cap).

The ecosystem is made up of hundreds of thousands of sellers earnings $25k-$100M of revenues. These are primarily small businesses, run by operators who have found a category niche and built businesses that have scaled even further than many of the owners had expected. A breakdown of the market is here (I pulled this from a slide deck my colleague Sakib Jamal made):

The story isn’t perfect.

Amazon is full of horror stories. One of the first articles I used to point to people, while spending time on the space, was this article by The Verge: “Prime and Punishment.” There’s a ton of Blackhat and Greyhat activity that goes on. In many cases competitors might put fake negative (or positive) comments on your page to try and get an account de-ranked.

There are also stories of Amazon employees using data from their third-party sellers to help Amazon sell its own, competing products. Once per month the NY Times writes some story about how bad Amazon is to its third party sellers. I’m so glad they do, it’s given us a head start on spending time in the space, while many thought it was too risky.

But the reality is – while in some cases Amazon’s employees may try to compete with a third-party seller, it’s against Amazon’s guidelines and it’s rare. Amazon cares a lot more about proving it’s a highway for small business (and not getting broken up) than it does about selling soap better. The Amazon of today is different than it was yesterday.

And when it comes to getting de-ranked by Amazon, it’s worse for a small seller than a larger one. If a seller with ~$5M of revenues gets de-ranked due to some Blackhat activity, or a review claiming the product causes allergies… there is no customer service to call.

But for a larger account, or a seller who owns multiple accounts, they get assigned account managers. And so shut downs go from 60 days in length (due to the arduous appeals process) to 48 hours, which is much more manageable.

So while there are problems – they can be dealt with. And the tailwinds far outstrip them.

Amazon TPS are better versions of small businesses, because they have 3 superpowers

(1) They have a Compounding Comment and Review Moat. When an account has lots of positive reviews and comments, it increases the ranking. And the higher the ranking, the more comments and reviews an account will get, and so on. So with each comment/review, the account increases its defensibility in a compounding fashion.

a. It is very rare for small businesses to actually have compounding moats, but they exist here

b. The ranking moat on Amazon is better/different than being rankly highly on Google SEO, because the rules are more clear, and it’s easier to control for increasing the number of reviews/comments and sales that drive the ranking. Think of it similarly to owning real estate in a country where the government’s property laws are more clear than in a country where the laws move around.

(2) They have high margins. Which is counterintuitive. And these businesses often operate at 20%+ net margins. Why?

a. Because they don’t pay for their real estate. When you search for a product, a list of sellers/items comes up in the search result. Being ranked number 1 in a category is like having a corner store front on a busy street, without paying any rent for it. And having good reviews/comments is like having a nice view and big, wonderful windows. These accounts are basically like digital real estate.

(3) They have variable cost P&Ls. Because Amazon takes care of so much of the work on a variable basis (shipping, returns, inventory management etc) the expenses of the business are easier to manage.

Normal small businesses typically have high fixed costs, low margins, and low barriers to entry – yet they can borrow at single digit rates if they’ve been profitable long enough! Yet just because a business lives on Amazon, it’s thought of as “more risky.”

The “Platform Risk” on Amazon exists, but so does “scaffolding risk” of a NYC store’s storefront. Are you kidding me? Would you rather finance or own some little store on a random street than a high margin, variable cost, compounding moat business on Amazon?

These stores are growing

It used to be that every little town, in every little state, in every little country needed a store that sold XYZ. Hammers, nails, water bottles, dish soap, etc.

But now, every town is starting to shop at the same place. So these category leaders/TPS accounts are going to continue to see power laws among them, and go from being very small businesses, to very large ones.

There is a need for capital

But for now – there is not a lot of capital in the space, and many of these sellers cannot keep up with their own growth. The easiest way to get de-ranked is by running out of inventory, but a business that can’t get financed, is fully bootstrapped, and that is growing quickly (with holiday season volatility) will struggle to procure inventory financing, or other types of capital it needs. Some lenders are popping up in the space – but it’s still new.

And this is just the beginning

A lot of entrepreneurs and investors saw the Thras.io announcement and assumed the winner had already been crowned. But per Thras.io’s fundraising article, they still only do $300M of revenues.

That’s 0.15% of the market. Holy ****! And they’re already a unicorn. And the market is growing.

I think the first wave of Amazon winners will be in the third-party seller rollup space. Some will win certain categories, or geographies. Others will win by “paying a premium for top accounts” or a “discount for struggling ones.”

This is not going to be a “winner take all market” in part because Amazon probably wouldn’t let one company own the whole market. Otherwise it would stop being a marketplace all together – and Amazon would lose too much leverage. There needs to be many winners. But there is probably room for 100 $1B+ companies and by 2023 that still would only be 7.5% of the market.

We’re somewhere between the National Anthem being played, and the bottom of the first inning. But not much further.

What’s happening now?

A bunch of announcements of new fundings have happened. Heyday raised money from General Catalyst and Khosla. Heroes raised money in Europe. Perch raised money from Spark.

Companies like Mohawk are trying to use data to launch new products, and WeCommerce was launched by Tiny Capital.

And even more have happened that are yet to be announced. If you think the space is hot now, just wait until 2021.

The Entrepreneurs are amazing

One of the most surprising developments is the quality of the entrepreneurs in the space. Some of the best talent appears to be leaving ridiculously high paying jobs to go do this.

“Our smartest friends are starting companies in the biggest space we’ve ever seen.” That is a good formula. That sentence alone could be an investment thesis.

What will happen next?

I expect these third-party seller rollups will start to develop their own niches, and their own approach. Saying there can only be one is like saying there could only be one app in the app store. They’ll have to differentiate over time… but they will.

And new companies likely will form to service these sellers. Pricing data companies, Ad networks, Referral programs, Warehousing companies, etc.

While the first wave may be third-party seller rollups, the next wave could be software companies that power them. And more ancillary markets will come out of all this.

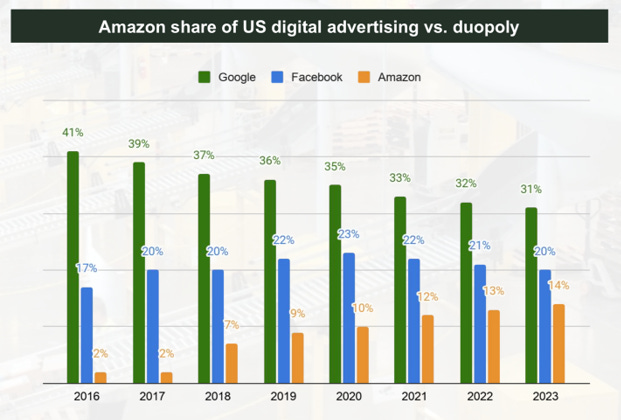

A shocking graph I saw recently was this one:

Source: eMarketer, Business Insider Intelligence 2019 report and Amazon Advertising 2020 report

Think about that! Amazon’s ad network is beginning to take meaningful market share compared to two of the other largest companies on the planet! In a growing market!

It’s like AWS, a thing Amazon was building right in front of all of us, but not broken out in its P&L on public filings – so not getting enough attention! And it’ll keep getting bigger as more of these third-party sellers begin to use it more actively. What’s amazing about this network is that it’s differentiated.

It had data about people’s shopping habits in a way Google and FB cannot offer to brands. The ROI on the network – in many cases, is higher than its incumbent counterparts and is building its own captive audience/customer base.

It’s yet another category that will be built, and be investable within the ecosystem.

When I talk to people in the space, they think I have crazy eyes. And anyone I talk to in the space who’s bullish, isn’t bullish enough. But realistically, these are higher quality versions of small businesses, being purchased as if they are distressed, shrinking ones. And the credit on them is solid – because the multiples on purchases are so low, that the debt is overly covered via excess cashflows. The yields are higher than lending to small businesses, yet much less risky.

Let me know if you’re spending time on an Amazon business of any kind.

Especially if you are building a third party seller rollup, a software company serving them, or anything in the Amazon ad agency space. I’m interested in hearing from you.

—

—

This is a personal blog collaboration. All views and opinions expressed are those of the authors, and do not reflect the views or opinions of any organizations the authors may be affiliated with. This website and the information contained herein is not intended to be a source of advice with respect to the material presented, and the information contained in this website does not constitute investment, tax, or legal advice. We make no representations as to the accuracy, completeness, correctness, suitability, or validity of any information on this site.

As an insider (selling on marketplaces since 2013), I couldn't agree more. We have groups of sellers (turnover in millions of dollars) still figuring out how to do taxation, packaging, and, logistics in India. It took 6 years to get a software solution which works for managing inventory and do payment reconciliation (still a lot of scope to build something like notion here), the whole seller ecosystem still has no solution for training the sellers on packaging according to their products. The businesses have grown to top million dollars in revenues but you see founders still discussing about how to ship products cheaply to warehouses. There are inefficiencies to be improved and of growing the whole ecosystem.

Love the article!

Reach out to me at aaron@samuraiseller.com - we manage millions of dollars of ad spend per month, through managed services and software, but started and still exist in PL space with a top 100 sellerratings.com account.

I agree with your sentiment. Anyone who is bullish isn't bullish enough! Amen! Would love to chat